ITD Cementation FY25 Results: Adani Group’s New Infrastructure Giant Aims for Strong Double-Digit Growth in FY26

ITD Cementation, now under the Adani Group, posts 18% revenue growth and 36% profit rise in FY25. With a ₹183 bn order book and ₹900 bn project pipeline, the company targets 25% growth in FY26.

ITD Cementation: Adani Group’s New Infrastructure Powerhouse with Ambitious Growth Plans

1. Introduction

In May 2025, India’s infrastructure space saw a significant reshuffle when Adani Group acquired a 67.5% stake in ITD Cementation, formerly part of Thailand’s ITD Thai Group. This strategic acquisition marks a pivotal moment for the EPC (Engineering, Procurement, and Construction) major, positioning it for larger projects and faster growth.

The company’s FY25 results reflect steady operational momentum, supported by a diversified order book and strong execution capability. With the Adani Group’s backing, ITD Cementation now has the financial muscle and strategic reach to expand aggressively in the coming years.

2. Company Overview

ITD Cementation is a leading infrastructure construction company in India, delivering end-to-end design, engineering, procurement, and construction services.

Core Business Areas:

- Maritime Infrastructure – Ports, harbors, jetties, and breakwaters.

- Water & Wastewater Projects – Pipelines, treatment plants, and water distribution.

- Hydropower – Dams, barrages, and related civil structures.

- Roads & Highways – Expressways, bridges, and interchanges.

- Railways & Metro – Elevated, underground, and station works.

- Urban Infrastructure – Buildings, industrial structures, and smart city projects.

The company’s portfolio reflects sectoral diversity, ensuring stability even when certain industries face slowdowns.

3. Shareholding Pattern (Post-Adani Acquisition)

- Adani Group: 67.5% (controlling stake)

- Foreign Institutional Investors (FIIs): Reduced from earlier levels to 9.2%

- Domestic Institutional Investors (DIIs): Down to 0.8%

- Public Shareholding: Balance held by retail and other investors

The decline in institutional stakes could be due to profit booking, portfolio rebalancing, or redeployment of capital to other opportunities — not necessarily a negative reflection on the company’s fundamentals.

4. FY25 Financial Performance

4.1 Revenue

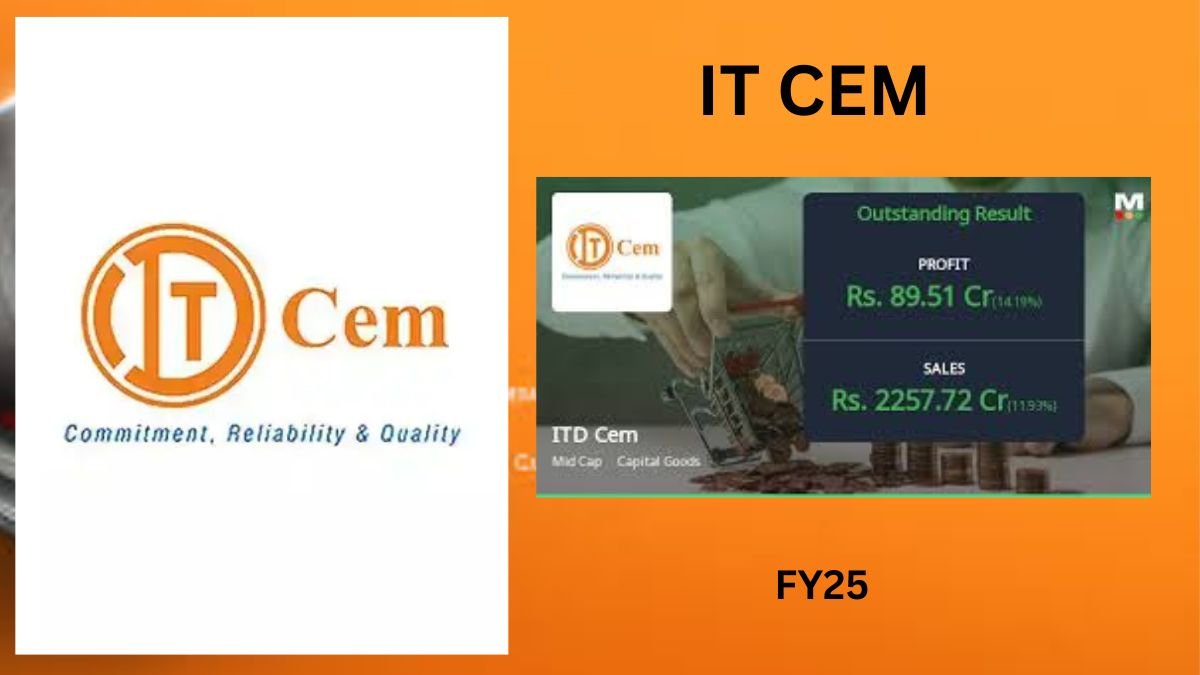

- Total revenue increased 18% year-on-year, reaching ₹91 billion.

- Growth supported by consistent project execution across marine, metro, and industrial sectors.

4.2 Profitability

- Profit After Tax (PAT): Up 36%, touching ₹3.7 billion.

- Margins improved due to cost control, efficient resource utilization, and favorable project mix.

4.3 Operational Highlights

- Timely execution of large-scale infrastructure projects.

- Strong cash flow generation, ensuring liquidity for ongoing works.

5. Order Book Strength

As of March 2025, ITD Cementation’s order book stands at ₹183 billion, providing revenue visibility for approximately two years.

Order Book Sector Mix:

- Marine Infrastructure: 35%

- Metro & Urban Transport: 18%

- Buildings & Industrial Projects: 25%

- Other Segments: Railways, hydro, and road projects making up the balance.

This sectoral and geographical diversification helps reduce risk and ensures steady revenue flow, even if one sector faces delays.

6. FY26 Targets and Strategic Goals

6.1 Growth Targets

- Revenue Growth: Aiming for 25% year-on-year increase.

- Profit Growth: Matching revenue growth at 25%, backed by higher-margin projects.

6.2 New Order Wins

- Targeting ₹150 billion worth of new projects in FY26.

- Large project pipeline worth ₹900 billion, with focus areas including:

- Mega port and harbor projects.

- Metro network expansions in tier-1 and tier-2 cities.

- Industrial infrastructure in manufacturing hubs.

7. Strategic Advantages Under Adani Group

Financial Capacity:

With Adani Group’s backing, ITD Cementation gains improved access to capital for bidding on and executing mega projects.

Expanded Market Reach:

The group’s presence in ports, logistics, and energy sectors opens doors for integrated project opportunities.

Operational Synergies:

Potential to collaborate with Adani Ports & SEZ, Adani Roads, and Adani Energy Solutions for bundled infrastructure solutions.

Brand Strength:

Being part of a large, globally recognized conglomerate enhances credibility for international tenders.

8. Industry Context and Growth Drivers

India’s infrastructure sector is witnessing unprecedented investment due to:

- Government Push: National Infrastructure Pipeline (NIP) and PM Gati Shakti Master Plan.

- Urbanization: Rapid metro network expansion in multiple cities.

- Maritime Growth: Sagarmala project and port modernization programs.

- Industrial Expansion: Demand for logistics parks, manufacturing zones, and industrial clusters.

These macro trends directly benefit EPC companies like ITD Cementation.

9. Potential Risks to Monitor

While the outlook is promising, certain challenges remain:

- Commodity Price Volatility: Steel and cement price fluctuations can affect project margins.

- Regulatory Delays: Approvals for large infrastructure works may slow execution.

- Execution Risks: Timely delivery is critical to avoid penalties and cost overruns.

- Competition: Intense bidding pressure in government tenders can squeeze margins.

10. Conclusion

ITD Cementation’s FY25 performance showcases operational efficiency, revenue growth, and a strong order pipeline. The acquisition by the Adani Group adds substantial financial and strategic leverage, positioning the company to capture a larger share of India’s booming infrastructure market.

With clear growth targets, a ₹183 billion order book, and a ₹900 billion project pipeline, ITD Cementation is entering a high-growth phase. Investors and industry watchers will be closely following how the company executes on its FY26 objectives and leverages its new parent group’s strengths.

For long-term growth prospects, the combination of diversified expertise, strong order book, and Adani Group backing makes ITD Cementation one of the infrastructure companies to watch in the coming years.

(Disclaimer: This article is for informational and educational purposes only. It does not constitute financial advice or a recommendation to buy or sell any securities. Please consult with a qualified financial advisor before making any investment decisions.)